Member Updates

Scroll down to see the following information about recent updates and practice reminders –

- Personal Tax Returns 2026

- Annual Accounting Jobs 2026

- Tax Forms 2026

- Tax Money 2027

- Practice Reminders

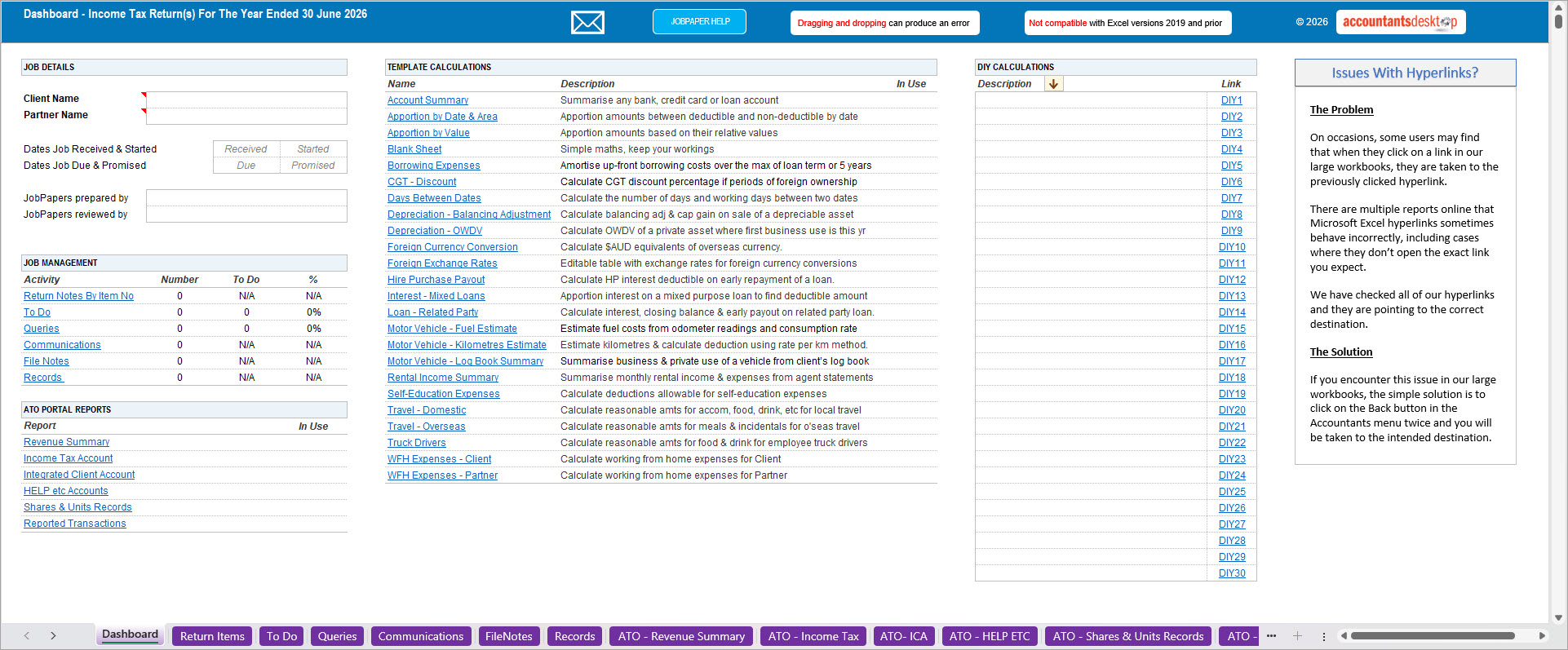

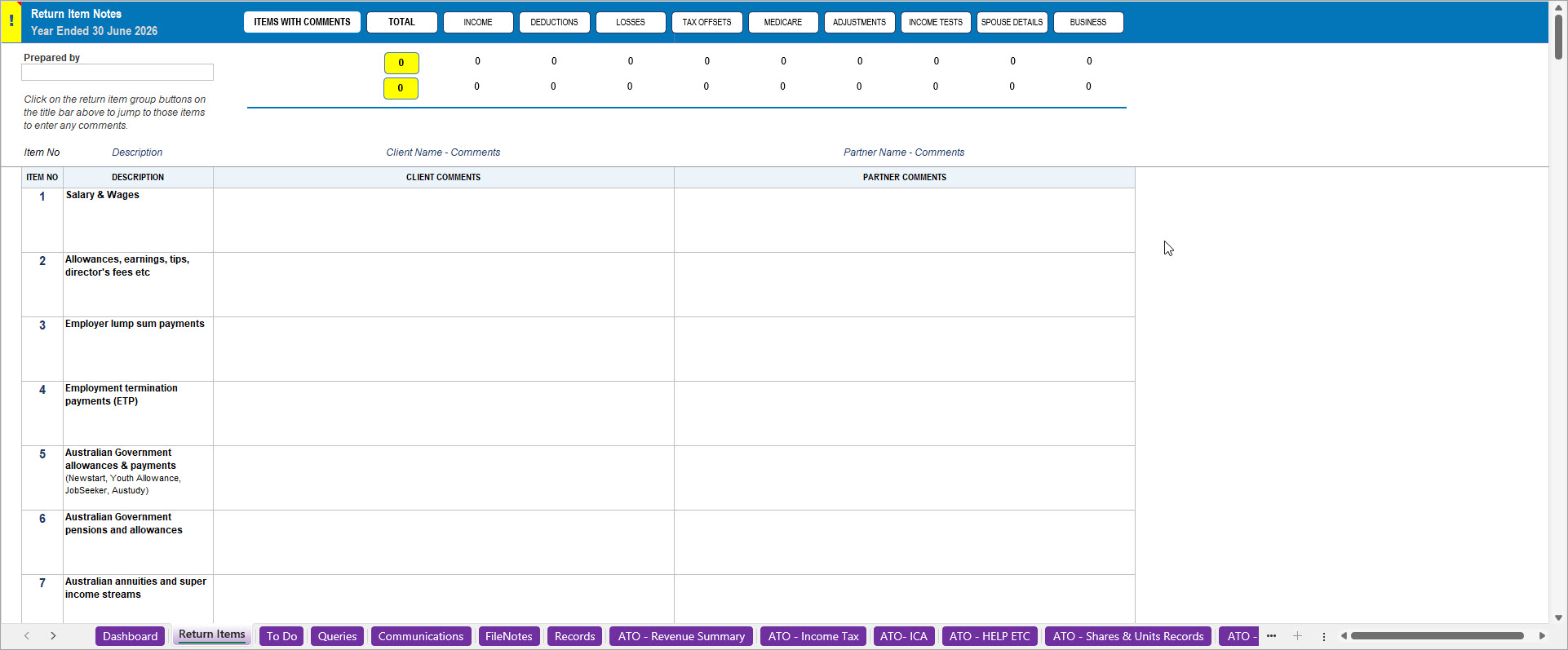

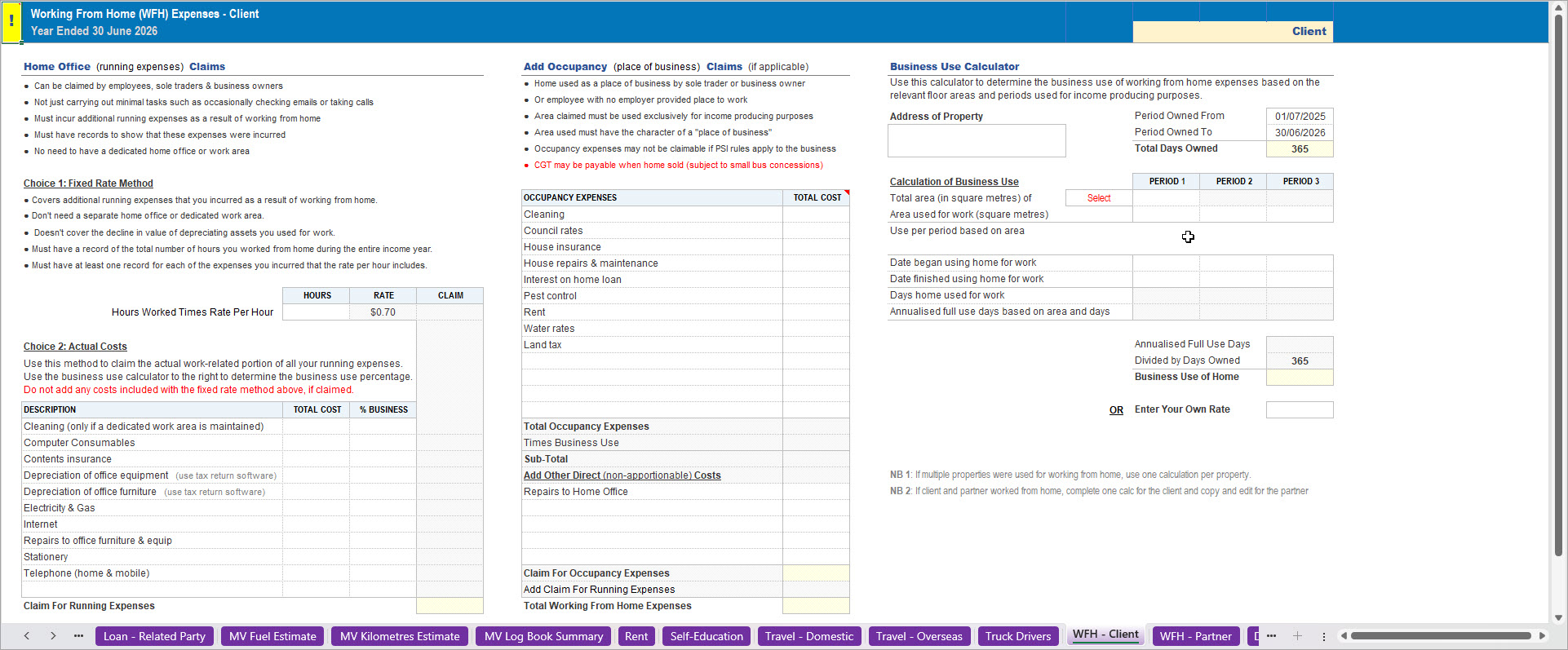

Our all-in-one Excel working paper solution for personal income tax returns for your client AND their partner for 2026 is now available for download.

And the 2026 versions of related tax forms can be downloaded from the Forms module. Each form includes PDF and Word versions of the following –

Interview – Personal Tax Return

Use this form to record notes during a client meeting where the information will be used to prepare their personal tax return later. While this may not be your usual workflow, most practices will need to handle this type of client interview from time to time.

Records Personal Return – Short

A concise one-page form you can send to your clients to help collect the information you need up front and reduce productivity-sapping delays caused by missing records.

Records Personal Return – Long

This 6-page version allows clients to provide detailed information about their income and expenses. It is best used selectively for clients who cannot attend your office and have the capacity to complete the form accurately.

Here’s a quick look at a few worksheets from the Excel workpaper –

Dashboard

Notes by item no

Work from home

4 July 2026

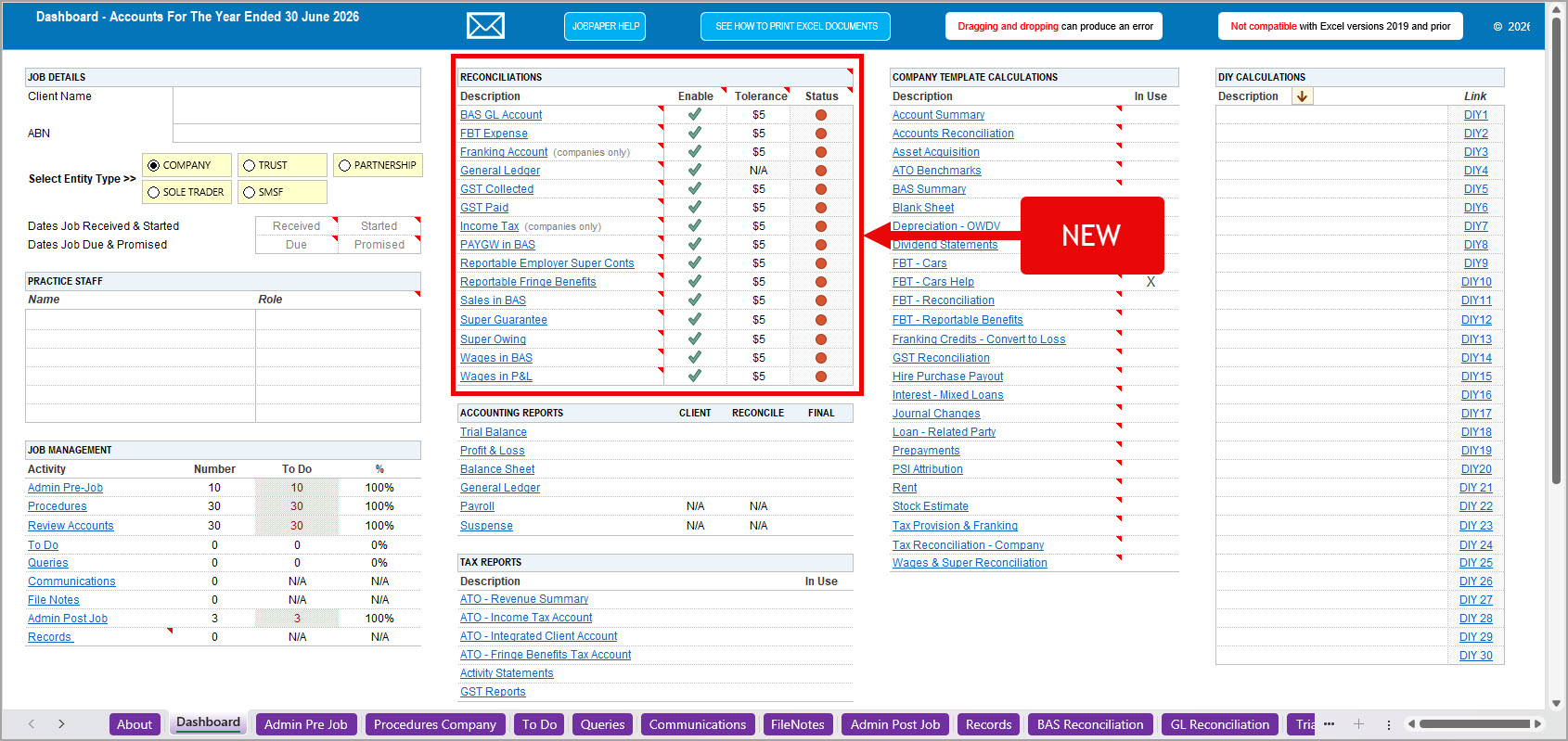

Our all-in-one Excel working paper solution for 2026 annual accounting jobs is now available for download and can be used for any entity type.

There have been some significant changes this year, including the following –

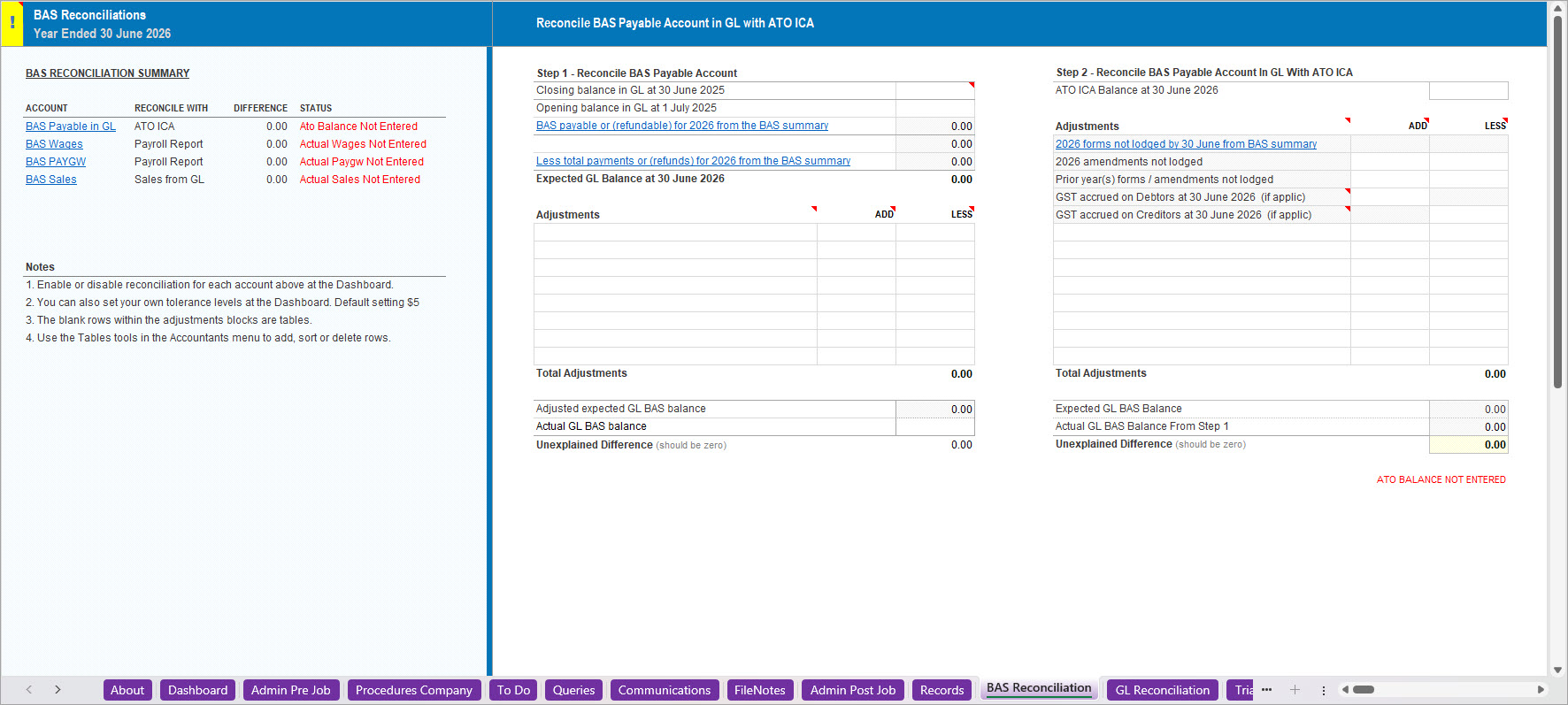

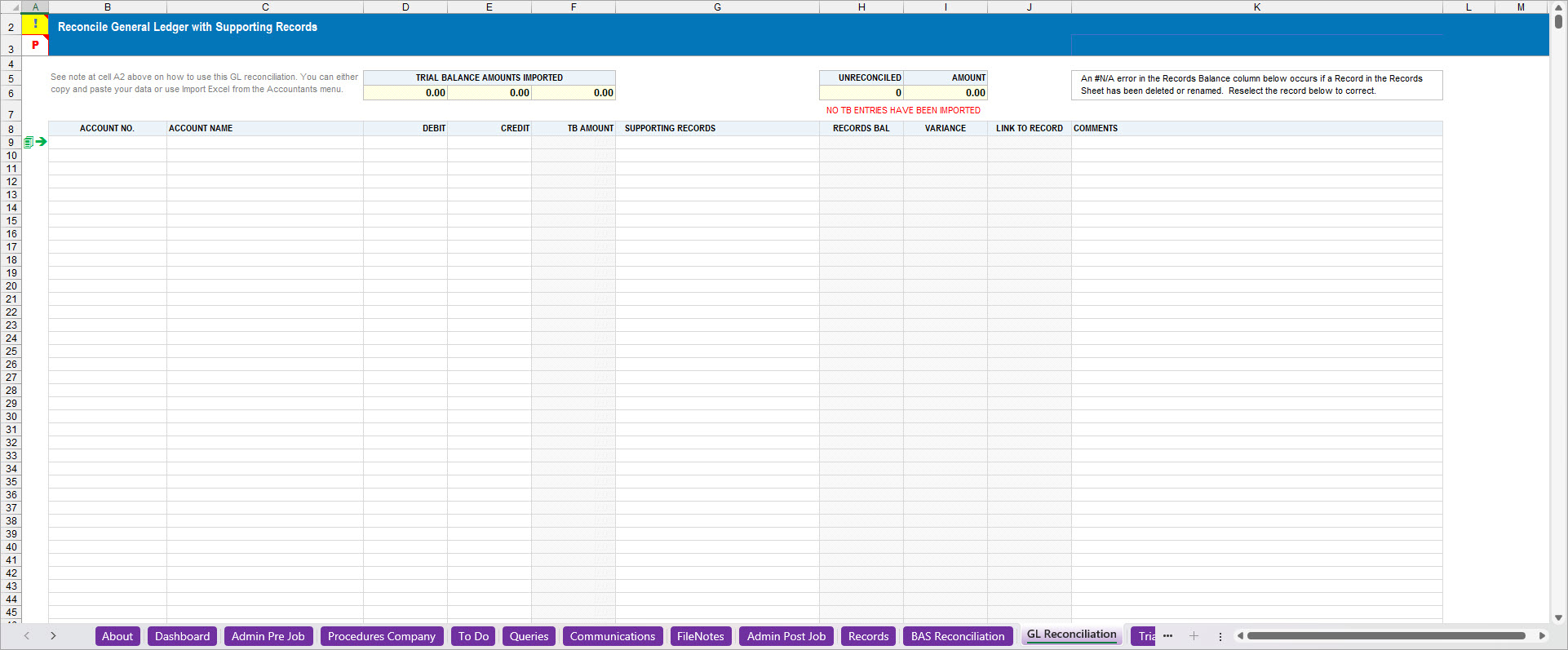

- New worksheet – BAS Reconciliation

- New worksheet – GL Reconciliation

- New worksheet – Journal Changes

- A greater focus on reconciliations, including centralised control with a summary on the dashboard

- ATO benchmarks updated to the 2026 release

Here’s a preview of some of these changes-

Dashboard

BAS reconciliation sheet

GL reconciliation sheet

4 July 2026

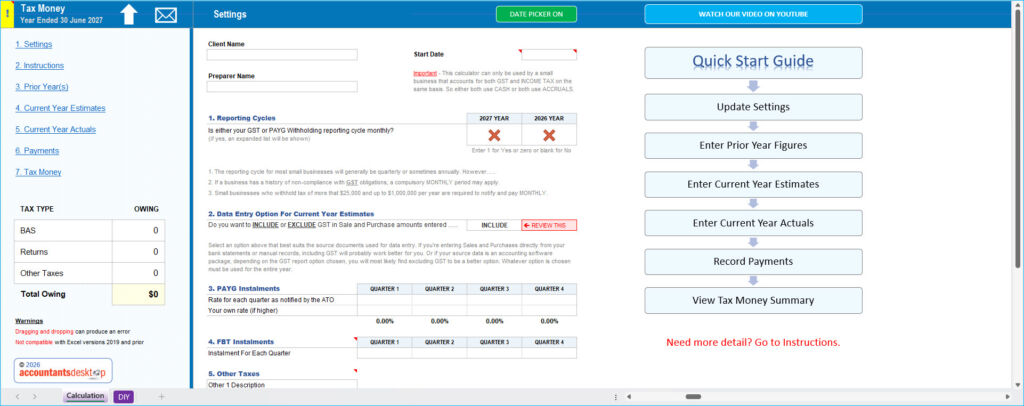

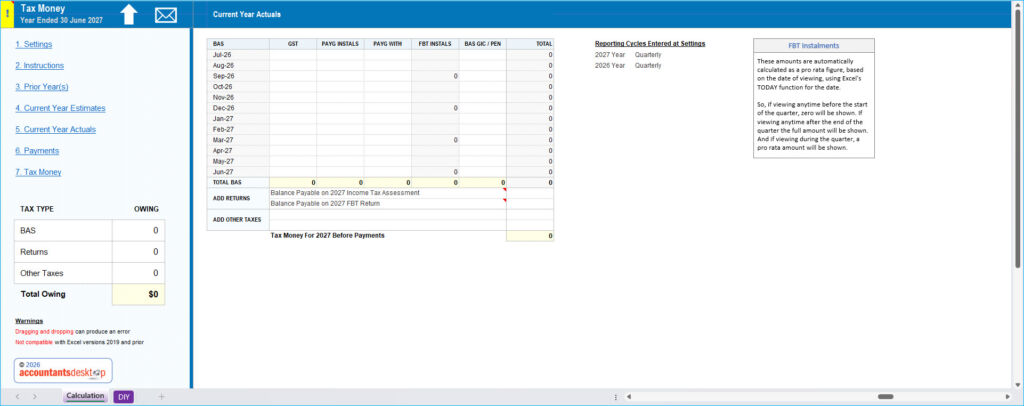

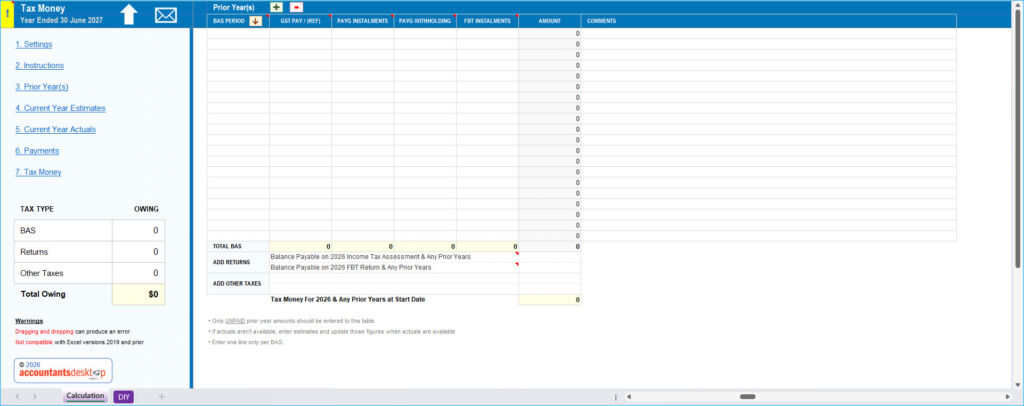

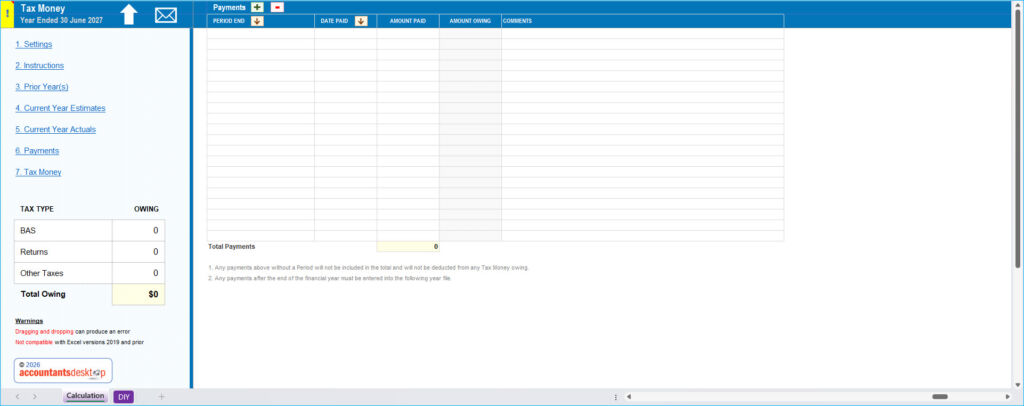

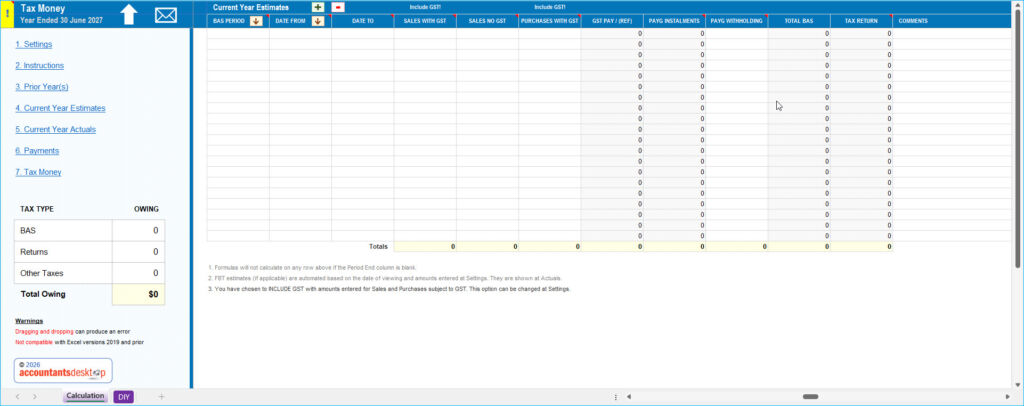

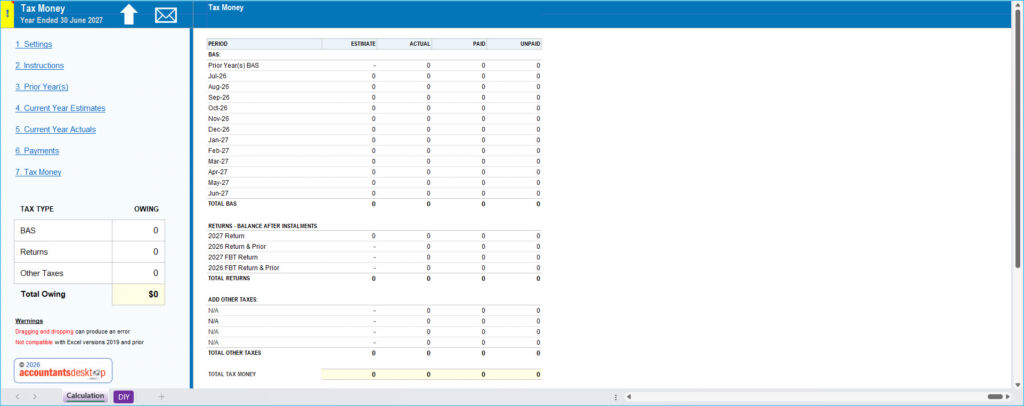

The 2027 version of this calculator is now available for download. It’s a good time to set up a system for those clients who need help managing their tax payments. Help them to avoid spending funds that aren’t truly available.

The ideal client types who would benefit from having their tax payments managed include –

- New businesses without a PAYG instalment rate.

- Growing businesses.

- Clients who generally struggle to meet their ongoing tax obligations.

Click on the thumbnails below to have a closer look at the latest version. Or click here to see our video on YouTube.

The file can be downloaded from Calculations/Budgets & Projections/Tax Money.

18 June 2026

Settings

Current Year Actuals

Prior Year

Payments

Current Year Estimates

Tax Money

Activity Statements

- Quarter 4 (April–June) PAYG instalment activity statement for head companies of consolidated groups – final date for lodgment and payment.

- June monthly activity statements – final date for lodgment and payment.

Finalising all your PAYG instalments before you lodge your tax return will ensure you receive the correct amount of credit in your income tax assessment.

Activity Statements

Quarter 4 (April–June) activity statements – final date for lodgment and payment.

Finalising all your PAYG instalments before you lodge your tax return will ensure you receive the correct amount of credit in your income tax assessment.

PAYG Instalments

Quarter 4 (April–June) instalment notices (forms R and T) – final date for payment and, if varying the instalment amount, lodgment.

Finalising all your PAYG instalments before you lodge your tax return will ensure you receive the correct amount of credit in your income tax assessment.

Superannuation for quarter 4, 2026

Due date for payment of super guarantee contributions for quarter 4 (1 April – 30 June 2026)

- Super guarantee contributions need to reach your employee’s super fund by this date – it’s important that you leave enough time for your super payments to reach and be processed by your employee’s super fund, especially if you’re using a clearing house.

- If you don’t pay minimum super guarantee contributions for quarter 4 by this date, you must lodge a Superannuation guarantee charge statement – quarterly and pay the super guarantee charge to us by 28 August 2026 to avoid additional penalties.

- You can’t offset contributions you have paid late for this quarter.

The quarterly super guarantee charge is more than the super guarantee you would have normally paid and is not tax deductible.

GST instalments

Quarter 4 (April–June) instalment notices (forms SA and T) – final date for payment and, if varying the instalment amount, lodgment.

TFN Report

Quarter 4 (April–June) TFN report for closely held trusts for TFNs quoted to a trustee by beneficiaries – final date for lodgment.

Foreign Account Tax Compliance Act (FATCA) Report

The reporting period for the FATCA is 1 January to 31 December. The due date for the report is 31 July the following year.

Common Reporting Standard (CRS) Report

Reports from Australian RFIs include data from January to December and are due annually, by 31 July in the following year.

Global and domestic minimum tax

The Global and domestic minimum tax return and the GloBE Information Return are due 31 July 2026 for fiscal years ending on or before 31 January 2025.

Activity statements

- Quarter 4 (April–June) activity statements lodged electronically – final date for lodgment and payment

- refer to Lodging your activity statements online for information on your eligibility for this later due date

- finalising all your PAYG instalments before you lodge your tax return will ensure you receive the correct amount of credit in your income tax assessment.

PAYG Withholding

- PAYG withholding payment summary annual report – final date for lodgment

- use this to summarise all payments to your employees and other payees and the amounts withheld from salary and wages and other payments

- these amounts should have been reported at labels W1 and W2 on previous financial year activity statements.

Employee Share Scheme (ESS) annual report

- ESS annual report – final day for lodgment.

Activity Statements

- July monthly activity statements – final date for lodgment and payment.

GST

- Final date for eligible monthly GST reporters to elect to report GST annually.

Taxable payments annual report

- Taxable payments annual report due for lodgment for:

Superannuation for quarter 4, 2026

- Lodge and pay quarter 4 (1 April – 30 June) Superannuation guarantee charge statement – quarterly if you did not pay your contributions on time for this quarter to avoid additional penalties

- For quarter 4, you can’t offset contributions you have paid late. See Missed and late super guarantee payments for more options on late contributions for this quarter.

- You can’t claim an income tax deduction for the quarterly super guarantee charge.

News

Lookup

2026 Return Forms & Instructions

| Individuals Return Instructions Supp Return Supp Instructions | Partnerships Return Instructions | Trusts Return Instructions |

| Companies Return Instructions | SMSFs Return Instructions | FBT 2026 Return Instructions |

2026 Resident Individual Tax Rates

| Taxable Income | Tax + Rate on Margin |

|---|---|

| $0 – $18,200 | NIL + NIL |

| $18,201 – $45,000 | NIL + 16% |

| $45,001 – $135,000 | $4,288 + 30% |

| $135,001- $190,000 | $31,288 + 37% |

| $190,001 and over | $51,638 + 45% |

| Plus Medicare Levy of 2% subject to thresholds |

Work Deductions

| Deduction | 2026 | 2025 |

|---|---|---|

| Motor Vehicle Cents Per Km | 88 cents | 88 cents |

| Work From Home – Fixed Rate Method | 70c/hour | 70c/hour |

| Overtime Meals Per Meal | $38.65 | $37.65 |

| Home Laundry – Work Clothes | $1/load | $1/load |

| Home Laundry – Mixed Load | 50c/load | 50c/load |

Superannuation Contribution Caps & Limits

| Component | 2027 | 2026 | 2025 |

|---|---|---|---|

| Concessional | $32,500 | $30,000 | $30,000 |

| Non-Concessional | $130,000 | $120,000 | $120,000 |

| Downsizer Limit | $300,000 | $300,000 | $300,000 |

Other Rates

| Item | 2027 | 2026 | 2025 |

|---|---|---|---|

| CGT Improvement Threshold | $194,165 | $187,962 | $182,665 |

| Car Depreciation Limit | $69,883 | $69,674 | $69,674 |

| FBT Rate | 47% | 47% | 47% |

| Division 7A Interest Rate | 8.77% | 8.37% | 8.77% |

| Superannuation Guarantee | 12.00% | 12.00% | 11.50% |