Member Updates

Scroll down to see the following information about recent updates and practice reminders –

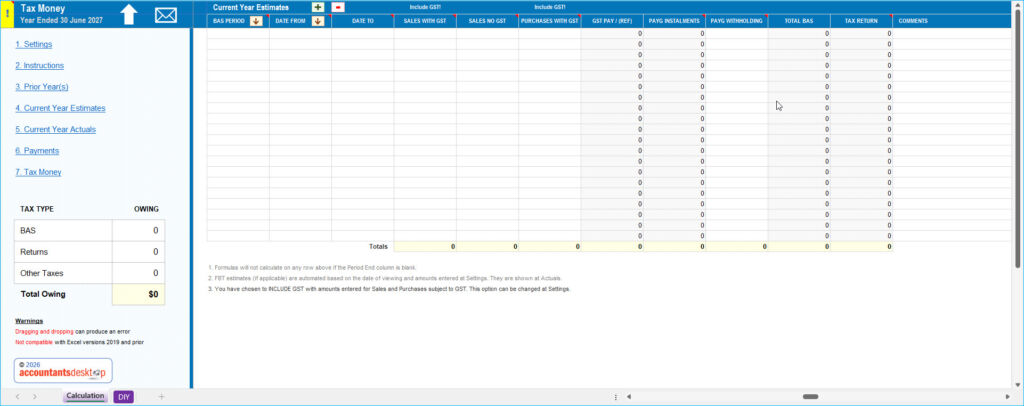

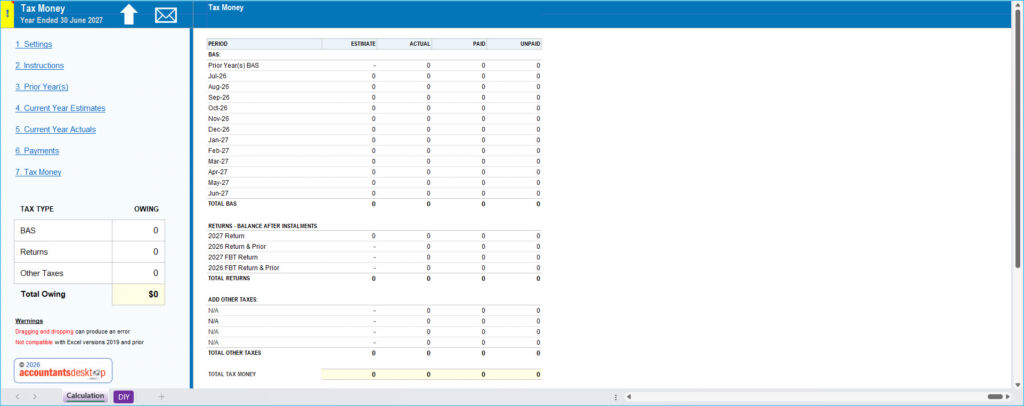

- Tax Money 2027

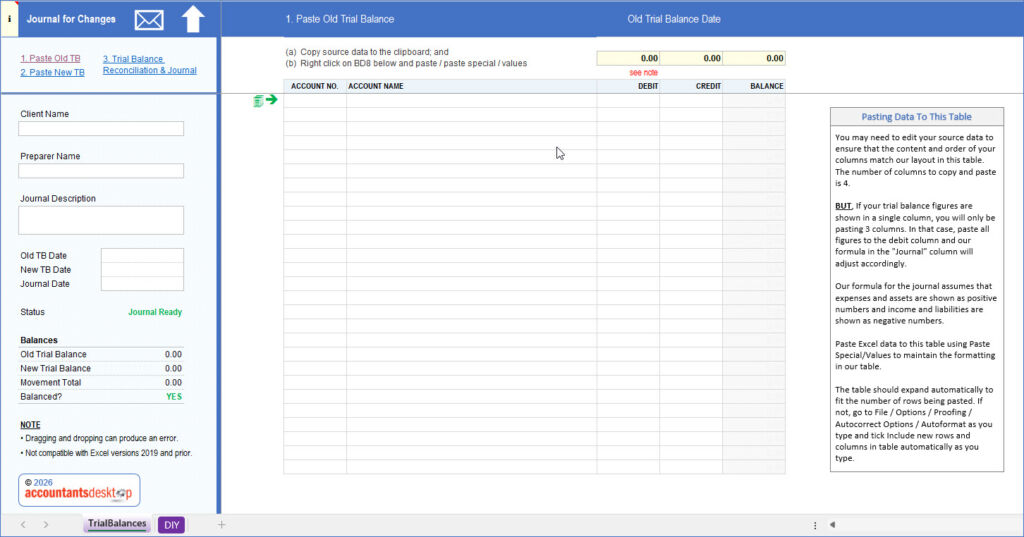

- Journal For Changes 2025

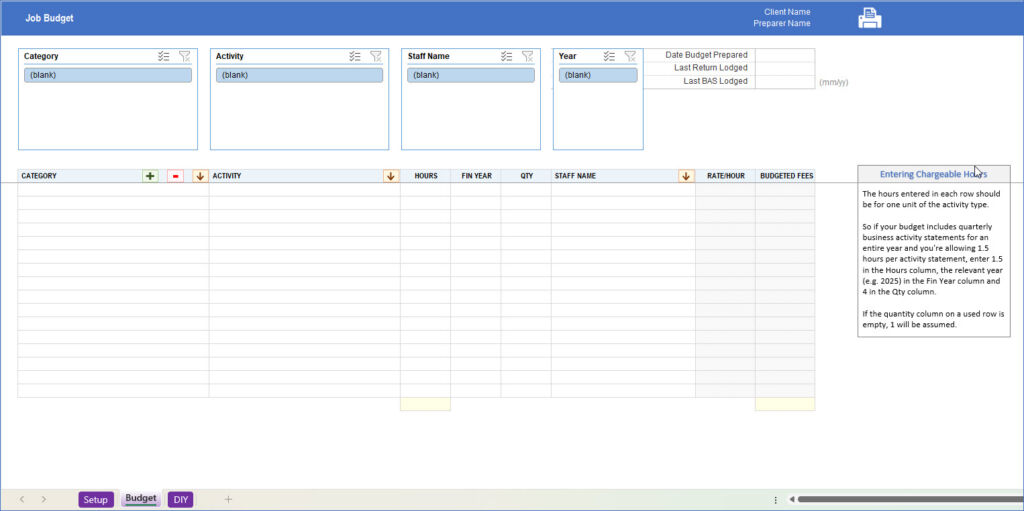

- Job Budget 2026

- Practice Reminders

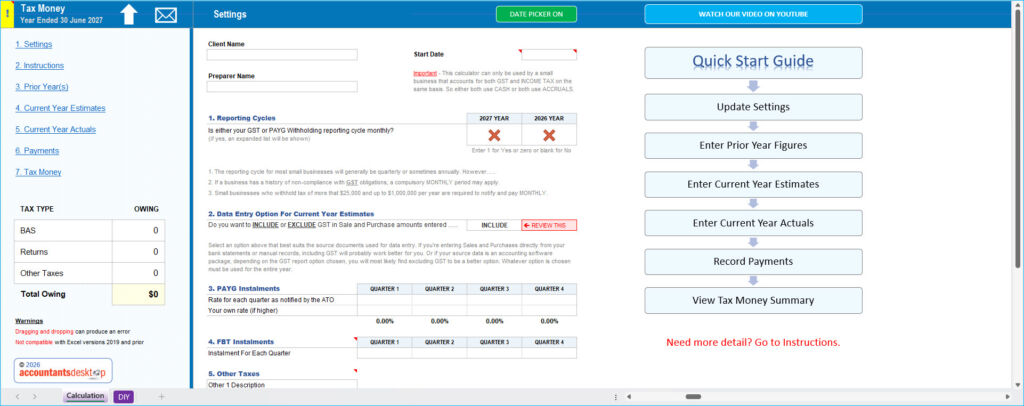

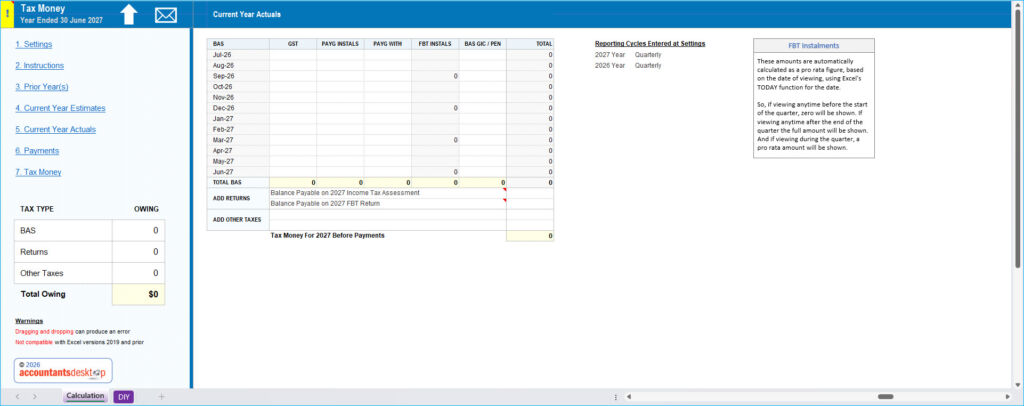

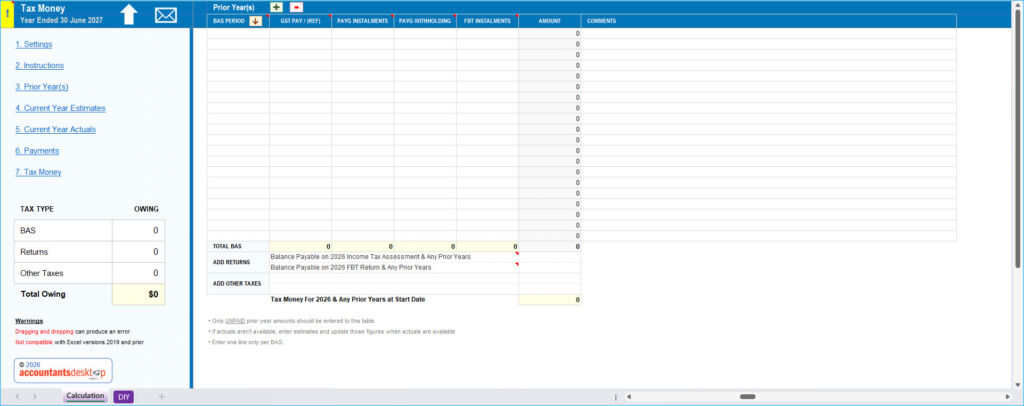

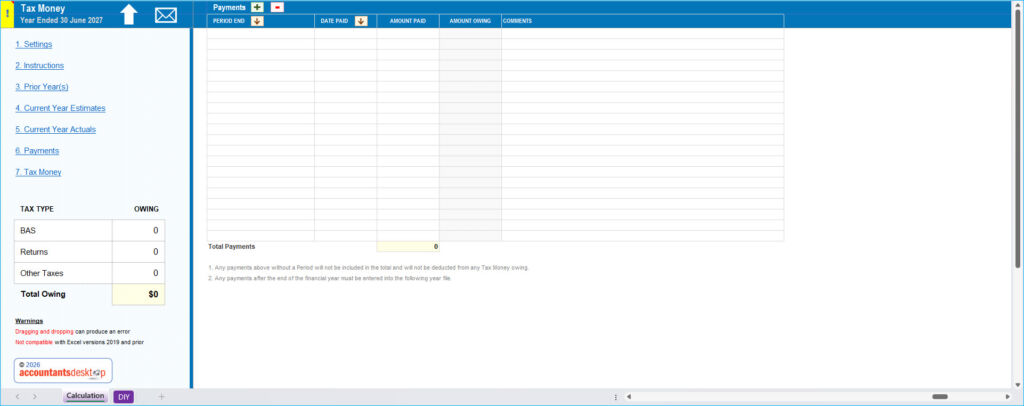

The 2027 version of this calculator is now available for download. It’s a good time to set up a system for those clients who need help managing their tax payments. Help them to avoid spending funds that aren’t truly available.

The ideal client types who would benefit from having their tax payments managed include –

- New businesses without a PAYG instalment rate.

- Growing businesses.

- Clients who generally struggle to meet their ongoing tax obligations.

Click on the thumbnails below to have a closer look at the latest version. Or click here to see our video on YouTube.

The file can be downloaded from Calculations/Budgets & Projections/Tax Money.

18 June 2026

Settings

Current Year Actuals

Prior Year

Payments

Current Year Estimates

Tax Money

We have redesigned this workbook to allow easier copy and paste of trial balances whether they be one column or two.

15 April 2026

This workbook has been re-designed for easier budgeting. Apart from the new layout, you can now filter on key components of the budget and calculate a budget for, or quote on, a multi-year job.

11 April 2026

Income Tax Returns

Lodge tax returns due for individuals and trusts with a lodgment due date of 15 May 2026 provided they also pay any liability due by this date.

Lodge tax return for companies and super funds with a lodgment due date of 15 May 2026 provided both the prior year and current year return will be non-taxable or result in a refund.

Note:

- This is not a lodgment due date but a concessional arrangement where failure to lodge on time (FTL) penalties will not apply if you lodge and pay by this date.

- Large and medium taxpayers and head companies of consolidated groups are excluded from this concession.

Activity Statements

Lodge and pay May 2026 monthly business activity statement.

FBT Return

Lodge and pay 2026 Fringe benefits tax annual return for tax agents if lodging electronically.

Super Guarantee Contributions

Super guarantee contributions must be paid by this date to qualify for a tax deduction in the 2025–26 financial year.

Child Care Subsidy and Family Tax Benefit Payments

If any of your clients receive Child Care Subsidy and Family Tax Benefit payments from Services Australia, the client and their partner must lodge their 2024–25 tax return by 30 June 2026, regardless of any deferrals in place. For more information, see the Services AustraliaExternal Link website.

News

Lookup

2026 Return Forms & Instructions

| Individuals Return Instructions Supp Return Supp Instructions | Partnerships Return Instructions | Trusts Return Instructions |

| Companies Return Instructions | SMSFs Return Instructions | FBT 2026 Return Instructions |

2026 Resident Individual Tax Rates

| Taxable Income | Tax + Rate on Margin |

|---|---|

| $0 – $18,200 | NIL + NIL |

| $18,201 – $45,000 | NIL + 16% |

| $45,001 – $135,000 | $4,288 + 30% |

| $135,001- $190,000 | $31,288 + 37% |

| $190,001 and over | $51,638 + 45% |

| Plus Medicare Levy of 2% subject to thresholds |

Work Deductions

| Deduction | 2026 | 2025 |

|---|---|---|

| Motor Vehicle Cents Per Km | 88 cents | 88 cents |

| Work From Home – Fixed Rate Method | 70c/hour | 70c/hour |

| Overtime Meals Per Meal | $38.65 | $37.65 |

| Home Laundry – Work Clothes | $1/load | $1/load |

| Home Laundry – Mixed Load | 50c/load | 50c/load |

Superannuation Contribution Caps & Limits

| Component | 2027 | 2026 | 2025 |

|---|---|---|---|

| Concessional | $32,500 | $30,000 | $30,000 |

| Non-Concessional | $130,000 | $120,000 | $120,000 |

| Downsizer Limit | $300,000 | $300,000 | $300,000 |

Other Rates

| Item | 2026 | 2025 | 2024 |

|---|---|---|---|

| CGT Improvement Threshold | $187,962 | $182,665 | $174,465 |

| Car Depreciation Limit | $69,674 | $69,674 | $68,108 |

| FBT Rate | 47% | 47% | 47% |

| Division 7A Interest Rate | 8.37% | 8.77% | 8.27% |

| Superannuation Guarantee | 12.00% | 11.50% | 11.00% |